Shah Gilani: Here's a question for you: Has higher education become another great American scam?

I'm not talking about the rich getting scammed. They get what they pay for. They can afford to be scammed, and they don't wind up saddled with student loan debt after they graduate.

A lot of rich people send their kids to expensive private colleges hoping they'll get a good education that will lead them into their chosen careers. If they haven't chosen a career, rich parents are more than happy to give their kids the "experience" of college, with all its social aspects, country club accommodations, and alumni status.

Have you ever wondered how billionaires continue to get RICHER, while the rest of the world is struggling?

"I study billionaires for a living. To be more specific, I study how these investors generate such huge and consistent profits in the stock markets -- year-in and year-out."

CLICK HERE to get your Free E-Book, "The Little Black Book Of Billionaires Secrets"

But then there are kids who want a higher education because they believe a college education is their ticket to gainful employment and well-compensated careers. They pay for it themselves, or their hardworking parents cosign on loans or take out personal loans on behalf of their kids' college dreams.

For them, higher education is increasingly looking like a scam.

Some critics complain that this is students' own fault, that they're pursuing the wrong majors. Or they say that colleges themselves are lacking, that they're not teaching what kids need to know in our ever-changing economy.

However, my problem isn't with education or kids' choices. Today I'm telling you where my beefs are – and why they're costing today's kids and their parents billions…

My First Beef: Astronomical Student Loan Debt

My first beef is with the come-ons that lure kids and their parents who can't afford college into indentured servitude.

Personally, I don't get what costs $10,000 a year (which is cheap these days) or $25,000 a year. And I especially don't get what costs $50,000 and higher a year.

Maybe if kids were guaranteed jobs that allowed them to pay off their loans, those crazy costs might be justifiable.

But there's no guarantee on jobs, and so those costs aren't justified.

Half of all kids who recently graduated colleges and universities are unemployed.

Outstanding U.S. student loan debt now exceeds $1.2 trillion.

Students are saddled with an average of more than $21,000 in debts. This takes into account both those who got out relatively early without a degree and graduates who can owe $100,000 and more – well into their 50s.

The judge's gavel is seen in court room 422 of the New York Supreme Court at 60 Centre Street Feb. 3, 2012. (REUTERS/Chip East)

Illinois Attorney General Lisa Madigan has launched lawsuits against two debt-settlement firms she says engage in predatory practices and scam people trying to get control of their student loan payments.

The lawsuits are the first ever launched by a state against firms that specialize in assisting with student loan repayment. The targeted firms are First American Tax Defense LLC of Park Ridge, Illinois, and Broadsword Student Advantage LLC, based in Frisco, Texas.

Madigan's lawsuits accuse the two companies of violating anti-fraud laws, and say the companies do little more than apply for free federal programs that borrowers could access on their own at no cost. For this service, they charge as much as $1199 up front, and in Broadsword's case may also charge a monthly fee of fifty dollars.

"Employing high-pressure sales tactics, Defendants target financially vulnerable consumers with student loan debt in Illinois, and throughout the United States," reads the case against First American Tax Defense. "Despite wide-ranging student loan relief services, such as the ability to secure lower student loan payments, remove wage garnishments, negotiate student loan debt forgiveness, and improve credit scores, Defendants do not have such capabilities."

The company is also accused of offering to help navigate a new program "just approved" by Congress called the "Obama Forgiveness Program," which does not currently exist.

The suit also claims that while First American represents itself as "a dedicated group of attorneys," the company in fact only employs a single licensed attorney, who rarely if ever interacts with customers.

Broadsword, meanwhile, is accused of having sales representatives tell consumers that they could eliminate all their student loan debt by paying a few hundred dollars up-front and then a $50 monthly fee for ten years, when there was no basis for such an offer. Instead, monthly fees were allegedly redirected into an investment advisory firm called Affordable Life Plans, allegedly for financial planning services customers did not know they were signing up for.

The lawsuits seek to have the companies' contracts canceled and fines in excess of $10,000 for each discovered violation of Illinois law.

The volume of student loans has risen enormously in the past decade, recently passing $1 trillion and beating out credit card debt as Americans' second largest source of debt behind home loans. Thanks in part to rising college tuition and a laggardly economy, about seven million people have defaulted on their student loans, and the number is rising. Unlike other debts, student loans cannot be discharged in bankruptcy except for particularly severe circumstances, meaning their burden can be particularly oppressive for those struggling to pay.

With so much money at stake and so many people falling behind on loans, scams have the opportunity to flourish. According to the Federal Trade Commission, complaints about abusive business practices by credit-services firms numbers in the hundreds of thousands every year, and several such companies, have been sued by the FTC itself. Madigan's lawsuits, however, appear to represent the first effort by a state to specifically reign in abuses related to student loans.

Representatives for the two accused companies could not be reached immediately for comment.

Content created by The Daily Caller News Foundation is available without charge to any eligible news publisher that can provide a large audience. For licensing opportunities of our original content, please contact licensing@ dailycallernewsfoundation.org.

CHICAGO (AP) — Illinois Attorney General Lisa Madigan filed lawsuits Monday against two companies she says are scamming people who are paying student loan debts.

The lawsuits, filed in Cook and Champaign counties, alleged "deceptive practices" for charging up-front fees for phony services or for services that are already free. The companies' advertisements on radio, online and signs affixed to lamp posts and fences offered student loan forgiveness or lowered payments, Madigan said.

"All of the alleged services that these operators provide, you can access yourself at no cost because they are free programs offered by the U.S. government," she said a Chicago news conference. "Too often, students do not know what options they have to repay or reduce their loan payments."

She said her office received dozens of complaints about Chicago-based First American Tax Defense LLC and Texas-based Broadsword Student Advantage LLC, and says there are likely many more people affected. Messages left at both companies Monday weren't immediately returned.

The companies allegedly charged people up to $1,200 up front for sham services. In one instance detailed in the lawsuits, First American allegedly advertised for an "Obama forgiveness program" that Madigan said isn't a government program. Broadsword circulated ads targeting professionals who are paying off loan debt, including teachers, nurses, government employees and firefighters, according to audio of the company's radio ads provided by Madigan's office.

The lawsuits alleged that the companies violate Illinois laws, including a 2010 act that bans companies from charging upfront fees for help with debt relief.

Student loan debt affects nearly 40 million Americans who have $1.2 trillion in outstanding debt, according to Madigan's office. In Illinois, student loan borrowers owe roughly $26,000 on average, according to Illinois Public Interest Research Group.

Madigan said her office will be aggressively targeting other companies that allegedly do the same. Previously, her office has sued for-profit colleges for "deceptive practices" that left numerous students with debt for degrees that failed to qualify them for certain types of jobs.

———

Follow Sophia Tareen at http://twitter.com/sophiatareen.

You must be logged in to leave a comment. Login | Register

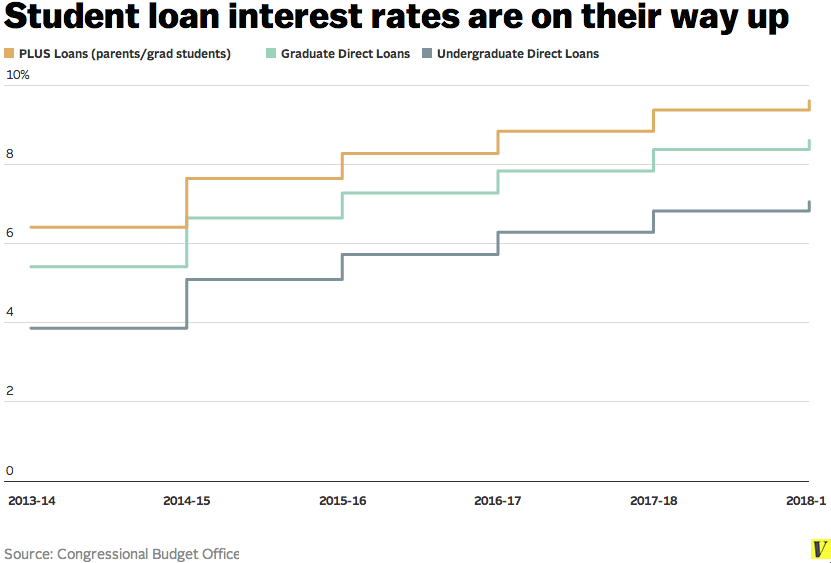

Student loan interest rates went up July 1 for the academic year that starts this fall. But unlike last year, there's no political uproar: Congress intended this to happen.

Student loans for undergraduates will have an interest rate of 4.66 percent, up from 3.86 percent last year. For graduate students, the interest rate on Stafford loans will be 6.21 percent, up from 5.41 percent.

PLUS loans, which are available to parents and graduate students and don't limit how much they can borrow, are more expensive, as always. The rate for those loans will be 7.21 percent, up from 6.41 percent last year.

Congress knew this would happen, and doesn't plan to change it

The interest rates are going up because last year Congress voted to tie student loan interest rates to market rates. In the past, interest rates were set by Congress and didn't have much relation to what borrowers were paying for other loans.

This is just the beginning of annual interest rate increases, according to the Congressional Budget Office. The interest rate on 10-year Treasury notes, which determines student loan interest rates, is projected to rise:

(The new interest rates actually came in slightly under these CBO projections, issued in May, but the overall trend still holds.)

And Congress isn't proposing to change this. Senate Democrats unveiled their vision for reauthorizing the Higher Education Act, the federal law that controls student financial aid, last week. It includes several provisions aimed at helping student loan borrowers control their debt, but the proposal wouldn't change how interest rates are calculated.

Instead, the focus has shifted to helping borrowers who can't afford their monthly payments.

Student advocates want a lower interest rate for everyone up front. But unless annual interest rate increases become politically untenable, that doesn't seem likely to happen.

In late 2008, Lance Cothern reunited with his high school girlfriend Tori after several years apart. Lance was almost ready to earn a bachelor's degree in accounting, and Tori was a sophomore studying nursing at a four-year public university at the time.

After a few years of dating, the conversations turned serious and they started planning a future together. Unfortunately, unbeknownst to either of them, Tori had a problem that was much bigger than she had ever realized – a lot of student loan debt.

Because of some scholarships and work during school, Lance managed to graduate college debt-free. That freed him up to focus solely on his future wife's debt, which eased the burden somewhat. However, as she pushed through her final semesters at school, they could only watch in horror as interest piled on top of interest to push her total burden up over $80,000.

The piling on of student loan debt

Yes, you read that right. Tori owed $80,000 for a bachelor's degree in nursing. Right about now, you're probably wondering how on Earth that happened.

Unfortunately, it's a lot more commonplace than you might think. In fact, Tori's student loan debt story isn't unlike any of the other tired old clichés relentlessly portrayed by the media: the struggling social worker who ends up 100K deep in student loans, the humanities Ph.D. who is forced to live with her parents well into her 30s, or even Kasey O., the woman I wrote about last year who still owes over $95,000 for a bachelor's degree in media arts and animation.

And just like many others who find themselves in this precarious situation, Tori didn't really know how much she had borrowed until it was far too late. Part of the problem, according to the pair, is that she went to college during the credit crunch, which temporarily made it difficult to access the most attractive student loans. So instead she took out loans with high or variable interest rates, with her largest balance teetering around 11 percent.

"To make matters worse, none of her student loans were subsidized," says Lance. "That means that her loans were charging her interest the entire time she was attending school. The interest would then be added to the principal of the loan and would incur even more interest charges over the course of her four-year college career."

Gulp.

Looking for a way out

Just like the many thousands of students stuck in this unfortunate situation, Lance and Tori wanted a way out. They wanted to begin a life together, and they didn't want to spend the best years of their lives struggling under the weight of nearly six figures of debt. After briefly researching income-based repayment and loan forgiveness options, Lance and Tori decided that their best option was to try to get out of debt as quickly as possible so they could move on with their lives. The prospect sounded daunting for sure, but they felt it was the best option they had.

The minimum payments on her student loans were around $700 per month, says Lance. "To pay off our debt, we lived frugally and used a very large percentage of our income to pay off her student loans, sometimes as high as 50 percent or more of our monthly income."

In an effort to earn more, Tori picked up some extra shifts at work and Lance switched to a less-demanding job with higher pay.

"We had to decide that some of life's conveniences would be put on hold while we paid the debt off," says Lance. "We didn't eat out often, we didn't have smartphones, we had a very small entertainment budget and we made sure we weren't wasting money on things that weren't more important to us than paying off her debt," he says. "Student loan debt had to be our No. 1 priority."

And it worked. In a matter of three years, the two focused almost all of their attention on completely annihilating her student loan debt. And now, in their late 20s, they've earned the right to start their adult lives with an entirely clean slate.

"For many 20- and 30-somethings, paying off the cost of college takes priority. Marriage, a house and family will have to wait," wrote Hadley Malcolm in USA Today, after sharing one of the saddest charts I've ever seen. A few highlights:

The percentage of college students who graduate with student loan debt was 65 percent in 2011, up from 46 percent in 1993

1 in 8 borrowers owes more than $50,000 for their education

The unemployment rate for recent college graduates was 13.3 percent in 2012

A whopping 16.9 percent of adults ages 25 to 34 reported moving back in with their parents in 2012

Note from editors: The Brookings Institution recently published a report that examined student loan debt between 1992 and 2010, and concluded that typical borrowers were no worse off now than they were 20 years ago. Interesting alternate viewpoint based on looking at the data differently…

Refusing to be a victim

But that's what makes Lance and Tori's story so intriguing. Just like so many other student loan debt horror stories, it has all the makings of a segment on the nightly news, but with a twist. Lance and Tori didn't allow themselves to become a pawn in the growing student loan debt crisis. They took control of their situation instead. Here's how they did it (and how you can do it too):

They used the debt snowball method. Made popular by Dave Ramsey, the debt snowball method for debt repayment requires you to focus your energy on either your loan with the smallest balance until it is paid off. Then you move on to the loan with the next lowest balance, and so on. "We paid off the highest rate first," says Lance. "Then we went loan by loan and decided which was most risky due to things like private vs. federal and fixed vs. variable rate."

They focused on earning more. One of the most efficient ways to pay off debt is to earn as much as possible. To do this, Tori picked up extra shifts at work and Lance focused on earning extra money on the side through freelance writing and starting a website, Money Manifesto. You can do the same by finding ways to make more money, whether it's freelancing, dog-walking, or babysitting. The end result is all that matters.

They kept their expenses low. Earning more only works if you're disciplined enough not to spend it elsewhere. To put as much money toward their loans as possible, Lance and Tori quit going out to eat and slashed their entertainment budget in half. They also lived a frugal lifestyle and went without many of the modern conveniences many of their friends had, like smartphones. Want to find a way to cut your expenses? Start by tracking your spending to see where your money is going in the first place.

Even though the journey was sometimes painful, the now debt-free twosome is glad they went through it.

"We learned a lot during the process," says Lance. "We learned that we could be happy even without a lot of money to buy things that many people consider necessities. We learned you have to take action or things will never get better," he says.

Lance and Tori's story proves that paying off a huge loan is possible, even over a short time frame, if you're willing to make it a priority. And, even though the steps they took might seem simple from a distance, the truth is, they're the only ones that work. It doesn't matter whether you're struggling with a giant mortgage, student loan debt, or credit card debt, the story is the same. Short of winning the lottery, you have to put in the work. You have to go without. You have to be willing to make sacrifices.

One of the basic tenets of GRS (and one of my favorite sayings) is that "no one cares more about your money than you do." And it's true.

I'd also add that "no one else can save you."

The painful truth is, sometimes you have to save yourself.

Are you still paying off student loan debt? What is your plan to pay it off once and for all?

Students, you may have to give up that grande mocha cappuccino once a month. Interest rates are rising on Tuesday for students taking out new loans, thanks to a bipartisan deal brokered by Congress and signed by President Obama. The deal tied rates to financial markets. Interest rates go from 3.86 to 4.66 percent on undergraduate Stafford loans. Graduate student loans go from 5.41 percent to 6.21 percent. Interest rates on Plus loans for parents go from 6.41 percent to 7.21 percent. For every $10,000 borrowed, the average borrower under the hike will pay back about $4 more every month when they begin paying back the money — about the price of a fancy latte. Buy that coffee, or pay the loan? Hmmm, tough choice.

It has come to our attention that the browser you are using is either not running javascript or out of date. Please enable javascript and/or update your browser if possible.

MEMORANDUM FOR THE SECRETARY OF THE TREASURY THE SECRETARY OF EDUCATION

SUBJECT: Helping Struggling Federal Student Loan Borrowers Manage Their Debt

A college education is the single most important investment that Americans can make in their futures. College remains a good investment, resulting in higher earnings and a lower risk of unemployment. Unfortunately, for many low- and middle-income families, college is slipping out of reach. Over the past three decades, the average tuition at a public four-year college has more than tripled, while a typical family's income has increased only modestly. More students than ever are relying on loans to pay for college. Today, 71 percent of those earning a bachelor's degree graduate with debt, which averages $29,400. While most students are able to repay their loans, many feel burdened by debt, especially as they seek to start a family, buy a home, launch a business, or save for retirement.

Over the past several years, my Administration has worked to ensure that college remains affordable and student debt is manageable, including through raising the maximum Pell Grant award by nearly $1,000, creating the American Opportunity Tax Credit, and expanding access to student loan repayment plans, where monthly obligations are calibrated to a borrower's income and debt. These income-driven repayment plans, like my Pay As You Earn plan, which caps a Federal student loan borrower's payments at 10 percent of income, can be an effective tool to help individuals manage their debt, and pursue their careers while avoiding consequences of defaulting on a Federal student loan, such as a damaged credit rating, a tax refund offset, or garnished wages.

While my Administration has made significant strides in expanding repayment options available to borrowers and building awareness of income-driven repayment plans, more needs to be done. Currently, not all student borrowers of Federal Direct Loans can cap their monthly loan payments at 10 percent of income, and too many struggling borrowers are still unaware of the options available to them to help responsibly manage their debt.

Therefore, by the authority vested in me as President by the Constitution and the laws of the United States of America, I hereby direct the following:

Section 1. Expanding the President's Pay As You Earn Plan to More Federal Direct Loan Borrowers. Within 1 year after the date of this memorandum, the Secretary of Education shall propose regulations that will allow additional students who borrowed Federal Direct Loans to cap their Federal student loan payments at 10 percent of their income. The Secretary shall seek to target this option to those borrowers who would otherwise struggle to repay their loans. The Secretary shall issue final regulations in a timely fashion after considering all public comments, as appropriate, with the goal of making the repayment option available to borrowers by December 31, 2015.

Sec. 2. Improving Communication Strategies to Help Vulnerable Borrowers. By December 31, 2014, the Secretary of Education shall develop, evaluate, and implement new targeted strategies to reach borrowers who may be struggling to repay their Federal student loans to ensure that they have the information they need to select the best repayment option and avoid future default. In addition to focusing on borrowers who have fallen behind on their loan payments, the Secretary's effort shall focus on borrowers who have left college without completing their education, borrowers who have missed their first loan payment, and borrowers (especially those with low balances) who have defaulted on their loans to help them rehabilitate their loans with income-based monthly payments. The Secretary of Education shall incorporate data analytics into the communications efforts and evaluate these new strategies to identify areas for improvement and build on successful practices.

Sec. 3. Encouraging Support and Awareness of Repayment Options for Borrowers During Tax Filing Season. By September 30, 2014, the Secretary of the Treasury and the Secretary of Education shall invite private-sector entities to enter into partnerships to better educate borrowers about income-based repayment plans during the tax filing season in 2015. Building off of prior work, the Secretaries shall further develop effective ways to inform borrowers about their repayment options during the tax filing season in 2015, as well as through personalized financial management tools.

Sec. 4. Promoting Stronger Collaboration to Ensure That Students and Their Families Have the Information They Need to Make Informed Borrowing Decisions. By September 30, 2014, the Secretary of Education, in consultation with the Secretary of the Treasury, shall develop a pilot project to test the effectiveness of loan counseling resources, including the Department of Education's Financial Awareness Counseling Tool. The Secretary of Education shall convene higher education experts and student-debt researchers to identify ways to evaluate and strengthen loan counseling for Federal student loan borrowers. Additionally, the Secretaries shall collaborate with organizations representing students, teachers, nurses, social workers, entrepreneurs, and business owners, among others, to help borrowers represented by these organizations learn more about the repayment options that are available to them in financing their investment in higher education and managing their debt, and to provide more comparative, customized resources to those borrowers when possible.

Sec. 5. General Provisions. (a) Nothing in this memorandum shall be construed to impair or otherwise affect:

(i) the authority granted by law to an agency, or the head thereof; or

(ii) the functions of the Director of the Office of Management and Budget relating to budgetary, administrative, or legislative proposals.

(b) This memorandum shall be implemented consistent with applicable law and subject to the availability of appropriations.

(c) This memorandum is not intended to, and does not, create any right or benefit, substantive or procedural, enforceable at law or in equity by any party against the United States, its departments, agencies, or entities, its officers, employees, or agents, or any other person.

(d) The Secretary of Education is hereby authorized and directed to publish this memorandum in the Federal Register.

If you are part of the beta test group, you will receive a link that will allow you to create a new password. If you are not part of the test group, you can learn more here.

President Obama declared 2014 a year of action – vowing to use the power of his pen and phone to help ensure that hardworking Americans have the opportunity to succeed. And this week will be no different. With a focus on supporting hardworking Americans and upholding our country's commitment to provide a quality education for all of our students, the President is again taking action. Today, he will deliver remarks at the White House, announcing new executive actions to further lift the burden of crushing student loan debt, including a Presidential Memorandum that will allow an additional 5 million borrowers with federal student loans to cap their monthly payments at just 10 percent of their income. A fact sheet detailing these new steps is below.

Tomorrow the President will do a live Q and A with Tumblr, answering questions directly from consumers across the country about this crucial issue. At both of those events, and throughout this week ahead of their upcoming vote, the President will use every opportunity to urge Congress to do their part by passing Senate Democrats' bill to help more young people save money by refinancing their federal student loans.

From reforming the student loan system and increasing Pell Grants to offering millions of students the opportunity to cap their monthly student loan payments at 10 percent of their income, making a degree more affordable and accessible has been a longtime priority for the President. But he knows there is much more work to do and that's what this week is all about.

FACTSHEET: Making Student Loans More Affordable

A postsecondary education is the single most important investment that Americans can make in their futures. Higher education results in higher earnings and a lower risk of unemployment, but for too many low- and middle-income families this essential rung on the ladder to opportunity and advancement is slipping out of reach. Over the past three decades, the average tuition at a public four-year college has more than tripled, while a typical family's income has barely budged. More students than ever are relying on loans to pay for college. Today, 71 percent of those earning a bachelor's degree graduate with debt, which averages $29,400. While most students are able to repay their loans, many feel burdened by debt, especially as they seek to start a family, buy a home, launch a business, or save for retirement.

The President and his Administration have a long track record of taking steps to make college more affordable and accessible for families. And as part of his year of action to expand opportunity for all Americans, the President is committed to building on these efforts by using his pen and his phone to make student debt more affordable and more manageable to repay.

Today the President will use the power of his pen to help millions of borrowers afford their student loan payments. He will sign a new Presidential Memorandum directing the Secretary of Education to propose regulations that would allow nearly 5 million additional federal direct student loan borrowers the opportunity to cap their student loan payments at 10 percent of their income. The Presidential Memorandum also outlines a series of new executive actions aimed to support federal student loan borrowers, especially for vulnerable borrowers who may be at greater risk of defaulting on their loans.

Today the President will also reiterate his call for the Senate to pass legislation that could help an estimated 25 million Americans refinance outstanding student loans at lower interest rates, the same as those available to federal student loan borrowers taking out loans this year. This move could save a typical student $2,000 over the life of his or her loans.

The Challenge of Student Debt: The challenges of managing student loan debt can lead some borrowers to fall behind on their loan payments and in some cases even default on their debt obligation, with such consequences as a damaged credit rating, losing their tax refund, or garnished wages. Because credit ratings are increasingly scrutinized in making employment offers, financing a home, or even opening a bank account, a damaged credit rating can further reduce borrowers' ability to repay their loans. Today's actions build on the Administration's significant progress in creating flexible repayment options for borrowers and raising awareness about the steps borrowers can take to responsibly manage their debt.

Capping Student Loan Payments at 10 Percent of Income: Today, the President will direct the Secretary of Education to ensure that student loans remain affordable for all who borrowed federal direct loans as students by allowing them cap their payments at 10 percent of their monthly incomes. The Department will begin the process to amend its regulations this fall with a goal of making the new plan available to borrowers by December 2015.

With legislation passed by Congress and signed by the President in 2010 and regulations adopted by the Administration in 2012, most students taking out loans today can already cap their loan payments at 10 percent of their incomes. Monthly payments will be set on a sliding scale based upon income. Any remaining balance is forgiven after 20 years of payments, or 10 years for those in public service jobs. However, this Pay As You Earn (PAYE) option is not available to students with older loans (those who borrowed before October 2007 or who have not borrowed since October 2011), although they can access similar, less generous options. No existing repayment options will be affected, and the new repayment proposal will also aim to include new features to target the plan to struggling borrowers.

This executive action is expected to help up to 5 million borrowers who may be struggling with student loans today. For students that need to borrow to finance college, PAYE provides an important assurance that student loan debt will remain manageable. Because the PAYE plan is based in part on a borrower's income after leaving school, it shares with students the risk of taking on debt to invest in higher education.

Many student loan borrowers are working and trying to responsibly make their monthly payments, but are nonetheless struggling with burdensome debt. For example, a 2009 graduate earning about $39,000 a year as a fourth year teacher, with student loan debt of $26,500, would have his or her initial monthly payments reduced by $126 under the President's Pay As You Earn plan compared with monthly payments under the standard repayment plan and would see a reduction in annual loan payments of over $1,500.

Doing All We Can to Help Students Repay their Loans: The President today will also direct the Secretaries of Education and the Treasury to work together to do all they can to help borrowers manage their student loan debts. Specifically, the Departments will:

Strengthen Incentives for Loan Contractors to Serve Students Well: The Department of Education administers the federal student loan program through performance-based contracts with private companies awarded through a competitive process. Rather than specifying every step of the servicing process, as was done in the guaranteed loan program that ended in 2010, these contracts provide companies with incentives to find new and innovative ways to best serve students and taxpayers and to ensure that borrowers are repaying their loans. Today, the Department announced that it will renegotiate its contracts with federal loan servicers to strengthen financial incentives to help borrowers repay their loans on time, lower payments for servicers when loans enter delinquency or default, and increase the value of borrowers' customer satisfaction when allocating new loan volume. These changes will improve the way that servicers are compensated to better ensure high-quality servicing for student loan borrowers.

Ensure Active-Duty Military Get the Relief They Are Entitled to: The Servicemember Civil Relief Act requires all lenders to cap interest rates on student loans – including federal student loans -- at 6 percent for eligible servicemembers. The Department of Education already directs its loan servicers to match their student borrower portfolios against the Department of Defense's database to identify eligible active-duty servicemembers. Now, the Department of Education will reduce those interest rates automatically for those eligible without the need for additional paperwork. It will also provide additional guidance to Federal Family Education Loan program servicers to provide for a similar streamlined process.

Work with the Private Sector to Promote Awareness of Repayment Options: The Secretary of the Treasury and the Secretary of Education will work with Intuit, Inc. and H&R Block, two of the U.S.'s largest tax preparation firms, to communicate information about federal student loan repayment options with millions of borrowers during the tax filing process — a time when people are thinking about their finances. The Administration is continuing its partnership with Intuit. through its TurboTax product, which serves around 28 million tax filers. The Administration will also form a new partnership with H&R Block, serving approximately 15 million tax filers through its 11,000 retail locations, and an additional 7 million tax filers through its digital tax products. Partnerships like these will give us the opportunity to provide information about federal student loan repayment, building upon our work during the most recent tax season by exploring different messages and the timing of information to best help borrowers in evaluating their federal loan repayment options.

In addition, the Administration will work with Intuit to explore ways to communicate with federal student loan borrowers through Intuit's free personal financial management product, Mint.com. Mint is used by 15 million people for financial management and advice, and partnering with Mint provides the opportunity to communicate with their 15 million users about income-driven repayment options. Mint includes the capability to provide personalized information about federal loan repayment options, based upon the information that a user has already provided to Mint.

Use Innovative Communication Strategies to Help Vulnerable Borrowers: Too many borrowers are still unaware of the flexible repayment options currently available to them, especially when they run into difficulties in managing their payments. The Department of Education is redoubling its efforts to identify borrowers who may be struggling to repay and provide them with timely information about their options supporting them through the repayment process and helping them avoid or get out of default. Last year, the Department's efforts led to more than 124,000 borrowers enrolling in an income-driven repayment plan like Income-Based Repayment or the Pay As You Earn plan Moving forward, the Department of Education will test new ways to reach 2.5 million borrowers with the greatest risk of encountering payment difficulty, such as borrowers who have left college without completing their education, missed their first loan payment, and those who have defaulted on low balances loans to get them back on track with their loan payments. The Department will also evaluate these strategies to identify which can be used on a larger scale and which are the most effective.

Promote Stronger Collaborations to Improve Information for Students and Families: All student borrowers are required to receive loan counseling when they first borrow federal student loans and when they leave school, but little is known about the effectiveness of these programs. Working with student debt researchers and student advocates, the Department of Education and the Department of Treasury will also develop and launch a pilot project to test the effectiveness of loan counseling resources, including the Department of Education's Financial Awareness Counseling Tool. The lessons learned will be considered for future actions by the Department and shared with outside partners like the National Association of Student Financial Aid Administrators to improve loan counseling activities at colleges and universities throughout the country. Another way to reach student borrowers is by working with professional associations to provide customized information about repayment options. Today, the Administration is announcing its commitment to work with the American Federation of Teachers, National Education Association, American Association of Colleges of Nursing, American Association of Nurse Practitioners, American Nurses Association, American Association of Physician Assistants, Business Forward, City Year, National Association of Social Workers, Physician Assistants Education Association, SEIU and the YMCA of the USA to provide comprehensive information about repayment options and federal student aid resources that are available to them. Moving forward, the Administration will continue to engage organizations, institutions of higher education, and others to ensure that all borrowers have access to the resources and information they need to responsibly manage the repayment of their student loans.

Additional Actions to Reduce Indebtedness and Promote College Affordability: Helping Students and Families Access Education Tax Benefits. In addition to helping borrowers manage their student loan debt, the Department of Education and the Department of Treasury will also work together to educate students, families, financial aid administrators, and tax preparers to ensure that all students and families understand what education tax benefits they are eligible for and receive the benefits for which they qualify. In 2009, the President created the American Opportunity Tax Credit (AOTC), which provides up to $2,500 to help pay for each year of college. But the process of claiming education tax credits like the AOTC can be complex for many students, including for the 9 million students who receive Pell Grants, and hundreds of millions of dollars of education credits go unclaimed each year. To help address this complexity, the Department of Treasury will release a fact sheet clarifying how Pell Grant recipients may claim the AOTC.

A money changer inspects U.S. dollar bills at a currency exchange in Manila January 15, 2014. REUTERS/Romeo Ranoco

Federal student loans will see the first of what could be several interest rate increases Tuesday, as a deal enacted by Congress last year takes effect.

Starting July 1 and continuing for the next year, all of the student loans offered by the federal government will see their interest increase by .8 percent.

Undergraduate Stafford loans, the cheapest offered, will raise from 3.86 percent interest to 4.66 percent. Graduate Stafford loans will go up to 6.21 percent from 5.41 percent, and the most expensive PLUS loans will rise from 6.41 percent to 7.21 percent. For every $10,000 in student loans taken out, that's an extra $80 a year in interest.

The increase is due to a rising rate of return on U.S. Treasury bills, to which the loans are now pegged. Until last year, student loan interest rates were set by law and did not adjust with economic conditions. Graduate Stafford student loans were stuck at 6.8 percent interest, while PLUS loans were at 7.9 percent.

Last year, the expiration of a previous congressional student loan deal briefly caused the interest rate for undergraduate Stafford loans to rise from 3.4 percent to 6.8 percent. Congress responded to public pressure by passing the Bipartisan Student Loan Certainty Act of 2013, which finally allowed student loans to adjust year to year in accordance with the Treasury bill.

The deal also lowered overall loan rates, down to 3.86 percent for undergraduate Stafford Loans, 5.41 percent for graduate Stafford loans, and 6.41 percent for graduate PLUS loans. As a result, even after Tuesday's increase, the top two tiers of student loans will remain cheaper than they were before.

However, if the economy improves, student borrowers could end up on the hook for higher interest payments than ever before. Even the cheapest Stafford loans will only cap out at 8.25 percent interest, and the PLUS loans can rise to over 10 percent.

Under the law, loan interest rates are fixed when the loan is taken out and do not continue to change later. That's a good thing for borrowers right now, when rates are rising, but if rates were to fall later graduates could find themselves stuck paying at higher rates.

That concern, plus the possibility of record-high rates in a stronger economy, made several activists worried when the reform bill passed last year.

The increase in interest rates could slightly help Democrats in the upcoming midterms, as they have decided to rally behind the issue of lowering student debt.

Democrats have tried to build grassroots support for a proposal by Massachusetts Sen. Elizabeth Warren that would alter the current student loan system by allowing borrowers to refinance down to lower interest rates. Warren's bill, however, wouldn't affect the current situation of rising rates.

Content created by The Daily Caller News Foundation is available without charge to any eligible news publisher that can provide a large audience. For licensing opportunities of our original content, please contact licensing@ dailycallernewsfoundation.org.

A former Blenheim man is auctioning off his student loan on Trade Me.

Daniel Moran, 24, of Christchurch, has tried a different approach to getting rid of his debt.

The former Marlborough Boys' College student completed a Bachelor of Information Technology at the Nelson Marlborough Institute of Technology in 2011.

He racked up about $36,000 worth of debt while studying away from home at the Nelson campus.

Over the past three years, he chipped away at the loan, which now sits at $26,508.34.

On Saturday, he was sitting at home going through his finances when he had an idea.

''I had my student loan bill in one hand and I was flicking through Trade Me at the same time,'' he said.

''I saw the section Cool Auctions and I thought I'd put a silly one up.''

He created a listing called ''student loan for sale!''. The listing appealed to anyone with too much spare cash to ''buy'' the remaining balance.

In return, the lucky buyer would get a photocopy of the payment receipt, a ''witty'' handwritten Christmas card every year, free technology advice, and a thank-you note.

The technology support analyst, who works for Harcourts in Riccarton, created the listing as a bit of fun, but he wasn't ruling out the possibility of someone actually buying it.

''There must be someone out there with a bit of spare money,'' he said. ''There could be worse things to spend it on.''

If the loan was paid off, he would save the percentage of his pay that was taken out of his bank account each month and put it towards travelling.

He was shocked the listing had already got almost 600 likes and 12 ''watchers'' in the three days it had been up, he said.

''Some people might think the idea is a bit silly, but it never hurts to think outside the box,'' he said.''

The top one per cent might have a lot of spare cash, and that's not a lot of money to them, but it's a lot to me.''

"It's inevitable at some point there will be a cap on student loan guarantees. And when that happens you're going to see a repeat of what we saw in the housing market: when easy credit for buying or flipping a house disappeared we saw a collapse in the price housing, and we're going to see that same collapse in the price of student tuition, and that's going to lead to colleges going out of business."

A majority of young Americans- 57% – view student loan debt as a major problem, and the average college student graduates with $30,000 in debt.

As Cuban and others point out, the failure to address these aspects will lead to diminished economic productivity in the long run, since young Americans have to spend a growing percentage of their income to service student loan debt.

When you factor in a high youth unemployment rate of 13.2%, you have an economic perfect storm that can decimate Millennials before they even get started.

President Obama has addressed the student loan crisis by targeting the symptoms: implementing measures to cap monthly payments, expand government grants and create tuition tax credits.

However, the President's "solutions" do not get to the roots of the problem: the rising cost of tuition and the unending supply of student loans that are paying for it.

Students hoping to become public defenders, work in the health field, or hopeful veterinarians in the state of Kentucky specializing in large food animals -- you're in luck.

You might be eligible for a number of programs that will help to repay your student loan debt. (Problem is, these programs aren't easy to find out about.)

"The information can be really buried within a website or can be fractured," said Betsy Mayotte, director of regulatory compliance at the nonprofit organization American Student Assistance. "You kind of have to dig for the details."

With the interest rate on new subsidized Stafford loans doubling from 3.4 percent to 6.8 percent on July 1, 2013, students taking on debt to pay for their graduate degrees might consider researching the different programs out there. To help guide students interested in forgiveness programs, ASA has put together an eBook called "60+ Ways To Get Rid Of Your Student Loans (Without Paying Them)." The organization divides the programs into two broad categories.

"Forgiveness programs are generally programs where you are rewarded for something that you do. Generally it's some sort or volunteer or a specific working profession where there's a need for people to work in that profession," said Mayotte. "Unfortunately, discharge is for when something bad happens to you."

The loan forgiveness and discharge programs were instituted by the federal government (as well as some state governments, organizations and private businesses) to eliminate all or part of a student's loans if he or she qualifies. Borrowers who give back to their community, work in fields or areas of need, or face unpredicted, extenuating circumstances are eligible for these different programs.

To apply for forgiveness, you may need proof that you've worked for the required number of years at the location or profession that makes you eligible for the program.

The types of loan forgiveness programs available can be divided among these broad categories:

Community service One community service option is applying for an AmeriCorps. award. It repays part of a person's student loans based on their service in the AmeriCorps program. The U.S. federal government program is meant to engage adults in intensive community service work with the goal of "helping others and meeting critical needs in the community." Other volunteer organizations offering loan forgiveness include the Peace Corps. and Volunteers in Service to America (VISTA).

Military Perhaps one of the most well-known ways to forgive your student debt. Generally there are two types of programs -- ones that pay for school while you're in school and then programs relating to existing loan forgiveness. You should speak with a recruiter about the different plans out there. Find out more information at Military.com.

Profession The most common professions eligible for loan forgiveness tend to be in the health and teaching fields. Mayotte says some states are really thirsty for nurses, doctors, teachers, or public defenders -- and may have forgiveness programs to attract those types of workers. You can find more career-based forgiveness programs with an online search or by talking to your employer. Find out more information at FinAid.org.

State specific You may be eligible for a program in a particular state if you are a legal resident in that state, work in one of the selected jobs, have a license for one of the jobs in the state, or went to school there. Search online to see what programs are available to you. Go to the state's website and search around. State specific programs can change or be eliminated based on budget, so keep an eye out.

Closed schools/school errors Borrowers may be eligible if their school closed while they were attending or within 90 days of leaving it. They may also be eligible if they withdrew from school and were not refunded the correct amount. Borrowers are only eligible if they received their loans on or after January 1, 1986.

Disaster There's a discharge option for spouses of eligible public servants or other eligible victims who died or became permanently and totally disabled due to physical injuries suffered as a result of the September 11, 2001 attacks.

Financial hardship Borrowers who face financial hardship based on income or debt could be eligible for these options:

Bankruptcy Contrary to popular belief, you can get rid of your loans in bankruptcy. But it's difficult to do so. You must prove to a bankruptcy judge that repaying your loans would be an undue hardship. This standard generally requires you to show that there is no likelihood of any future ability to repay. Learn more.

Income-based repayment To qualify you must have a partial financial hardship, which means that payments to your eligible loans exceeds 15 percent of your discretionary income. After 25 years -- 10 working in public service -- any student loan debt left over is forgiven. Learn more.

Income-contingent repayment Similar to the income-based repayment program, but payments are capped at 20 percent of discretionary income. Learn more.

Pay as you earn forgiveness Only for newer borrowers. You must be a new Direct Loan borrower as of October 1, 2007, with a disbursement made after October 1, 2011. Any Direct Consolidation loan made on or after October 1, 2011, that does not include a Parent PLUS loan or a loan made prior to October 1, 2007 is eligible. Learn more.

Fraud If someone fraudulently obtained the loan in your name you may be eligible to have your loan discharged.

Medical For borrowers who suffer from physical or mental impairments or have died.

Mayotte said it's important to note that for many of these loan programs, the amount that's forgiven can be taxed as income.

She says the best way to find out what programs are available to you is searching online and asking.

"Ask a potential employer if student loan repayment is part of a benefit. Ask a school that you're attending if the school is aware," says Mayotte. "I wouldn't be surprised if there were some super secret programs out there that weren't online."

Learn more about student loan forgiveness programs -- click play on the audio player above to hear the Marketplace Money interview with Mayotte.

Daryl Paranada is the associate web producer for Marketplace overseeing all daily website content and production, as well as producing multimedia features -- including the popular economic explainer series Whiteboard -- and special projects. Follow him on Twitter @darylparanada.

Personally, I don't get what costs $10,000 a year (which is cheap these days) or $25,000 a year. And I especially don't get what costs $50,000 and higher a year.

Personally, I don't get what costs $10,000 a year (which is cheap these days) or $25,000 a year. And I especially don't get what costs $50,000 and higher a year.

For more advice on dealing with your student loans check out these links:

For more advice on dealing with your student loans check out these links: